April 10, 2025

APRIL 2025 WASDE REPORT SUMMARY AND NOTES

The April WASDE report was viewed as neutral for corn, soybeans, and wheat. Given the uncertainty surrounding global trade and geopolitics, the following note was included in today’s commentary:

The WASDE report only considers trade policies that are in effect at the time of publication. Further, unless a formal end date is specified, the report also assumes that these policies remain in place.

Market attention will focus on planting progress across the Midwest and ongoing trade rhetoric.

Corn

The domestic 2024/25 corn balance sheet called for increased exports and smaller ending stocks. Feed and residual use was reduced by 25 million bushels based on disappearance during the December-February quarter as indicated in the March 31 Grain Stocks report. Exports were raised by 100 million bushels based on the pace of sales and shipments to date. Ending stocks were reduced by 75 million bushels from last month to 1.5 billion bushels. This was nearly identical to the average pre-report estimate of 1.506 billion bushels (1.405 to 1.605 billion range). Global corn production was increased and ending stocks were also increased to 287.7 million metric tons. This was slightly lower than the average pre-report estimate of 288 million metric tons (285 to 290 million range).

Corn exports increased on pace of shipments and sales year-to-date:

Soybeans

The domestic 2024/25 soybean balance sheet called for higher imports and crush and lower ending stocks. Soybean crush was increased by 10 million bushels on higher soybean meal domestic use and soybean oil exports. Soybean oil for biofuel was lowered based on pace to date. Soybean ending stocks were lowered by 5 million bushels from last month to 375 million bushels. This was slightly below the average pre-report estimate of 381 million bushels but within the range of estimates (320 to 413 million range). The global soybean balance sheet called for lower production and higher ending stocks. Brazil’s 2023/24 production was revised higher while the current crop year production was left unchanged for Brazil and Argentina. Global crush was raised in Brazil, Argentina, Ukraine, and the U.S. Global ending stocks were raised by 1.1 million metric tons to 122.5 million, mostly due to the EU and Brazil. Brazil’s increased stocks were attributable to the realization of larger old crop supply. This was slightly above the average pre-report estimate of 122 million metric tons but within the range of estimates (121 to 124 million range).

Soybean crush increased based on pace year-to-date:

Wheat

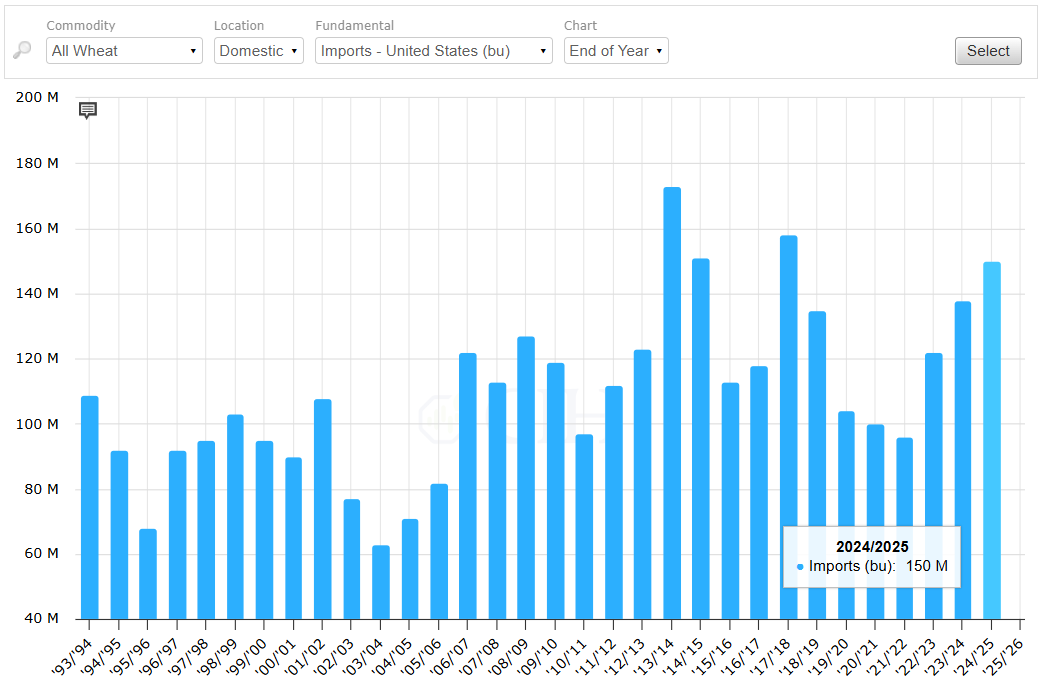

The domestic 2024/25 wheat balance sheet called for larger supplies, smaller use, and increased ending stocks. Imports were increased for Hard Red Spring, Durum, White, and Hard Red Winter varieties. Exports were lowered by 15 million bushels. Ending stocks were pegged at 846 million bushels, 27 million higher than last month and 22 percent higher than a year ago. This was also near the upper end of the range of analysts’ pre-report estimates (795 to 854 million range). Global wheat consumption was lowered from last month while ending stocks were forecast to increase. World consumption was lowered primarily on lower use in China and India. Exports were lowered for Russia, Australia, and the EU. World ending stocks were pegged at 260.7 million metric tons, nearly identical to the average pre-report estimate of 260.8 million metric tons.

If realized, wheat imports would mark highest level since 2017/18: